Remember your last online transaction.

Maybe you bought something from a grocery application, or maybe you ordered dinner from a food application.

You just tap a button, and the processing bar completes its journey, and after it, a pop-up appears: Payment successful.

But behind this faster payment, there is a system that connects to the banks, verifies your identity, checks for fraud, encrypts your card details, routes the transaction to the right bank, ensures the merchant gets money, and shows you confirmation instantly.

This system is called the Payment Platform

And without the support of a payment platform, online shopping, subscriptions, or even mobile banking would not be possible.

In this article, you will learn more about the payment platform, how it works, why it is important, and its features, with new trends and the right way to choose one.

Let’s start from the basics.

What is a Payment Platform?

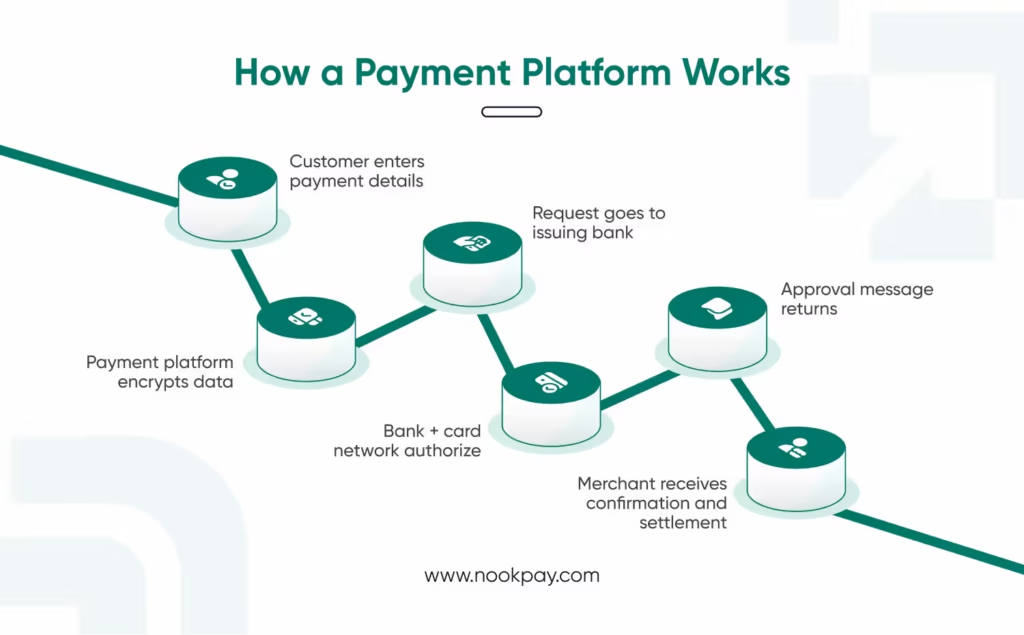

A payment platform is a digital system that helps businesses to send and receive digital payments smoothly and securely.

Whenever someone pays online, a platform acts as a middleman and handles the full journey — from collecting the card details to delivering the money into the merchant’s account.

Or we can say,

A platform is a digital cashier that manages millions of transactions at the same time.

A Payment Platform Does 4 Important Things –

A platform isn’t just a tool that accepts online payments. It actually performs four major tasks behind the scenes to make sure every transaction is smooth, safe, and successful.

1. Accepts Payment Information

This is the first step.

When a customer enters their card number, UPI ID, wallet details, or net banking credentials, the payment platform securely collects and encrypts this information.

The platform ensures:

- The data is captured correctly

- Nothing leaks to outsiders

- The user moves smoothly to the next step

Think of this as the digital version of handing your card to a cashier.

2. Processes the Payment

Once the platform collects the details, it sends them to the right places — banks, card networks (like Visa/Mastercard), or UPI rails.

During this step, the platform acts like a messenger between:

- The customer’s bank (issuer)

- The merchant’s bank (acquirer)

- The payment networks

It checks:

- Is the card valid?

- Is there enough balance?

- Is the payment allowed?

Then it returns the final answer — approved or declined — within a second.

3. Ensures Security and Fraud Checks

Every online transaction is scanned for suspicious behavior.

The platform uses tools like:

- AI-based fraud screening

- OTP or 3D Secure

- Device fingerprinting

- Encryption

- Tokenization

This prevents fraud, protects customers, and stops fake transactions before they cause damage.

4. Settles Money to the Business

After the payment is approved, the platform handles the behind-the-scenes banking work.

It ensures:

- The merchant gets the money on time

- Fees are calculated

- Transactions match bank statements

- Settlements follow T+1, T+2, or instant payout rules

This is like the final step where the cash reaches the business’s bank account.

What are the Core Components of a Payment Platform?

The payment platform is made up of multiple components that work together to make every transaction fast, safe, and successful. In this system, each component plays a specific role, and if one fails, the entire transaction flow is broken.

Here is the clear explanation of each component:

- Payment Gateway:

The payment gateway is an interface that users see at the time of payment. It collects users’ information like card numbers, UPI IDs, wallet details, and other important information, then encrypts it so the data stays safe.

It ensures that payments start smoothly, load quickly, and do not expose sensitive customer information.

2. Payment Processor:

Once the data is collected, the processor starts working. It communicates with the bank, the card network, and the payment partner to confirm whether the transaction should be approved or declined.

Without the payment processor, the transaction can not occur.

3. Fraud & Risk Management System

This component checks if the payment looks real or suspicious. Also, it analyzes device information, user location, past transactions, and more. To protect businesses from chargebacks, stolen cards, identity fraud, and suspicious activity.

4. Compliance & Security Layer

A payment platform must follow the global as well as local rules, such as PCI-DSS, KYC, AML, GDPR, and regional regulations.

Compliance ensures that businesses will stay legally safe, databases remain secure, and payments run without penalties or restrictions.

5. Settlement System

After the transaction is approved, the platform doesn’t settle the money instantly. It batches payments, calculates fees, and transfers funds to the merchant’s bank account after a scheduled timeline.

This system also gives businesses predictable cash flow and transparent payout cycles.

6. Reporting & Analytics Dashboard

The reporting dashboard is the control room of a payment platform.

It gathers every transaction in one place so businesses can see exactly what is happening across their payment flow in real time.

A strong dashboard doesn’t just show numbers, it gives insights like:

- Total transactions

- Approval and decline rates

- Refunds and chargebacks

- User behavior and payment patterns

- Revenue breakdown by method or geography

- Peak hours of successful payments

- Drop-off points in the checkout process

This helps operators understand how well their payment system is performing and where improvements are needed.

7. Integrations & APIs

Modern platforms offer APIs to connect websites, apps, CRMs, affiliate systems, or gaming platforms. APIs allow businesses to automate payment flows, pull transaction data, trigger refunds, or update user status without manual work.

How Payment Platforms Route Transactions?

When a user taps “Pay Now,” a lot of things happen in the background within 2–3 seconds.

A payment platform’s biggest job is to route the transaction through the safest and fastest path so the payment gets approved smoothly.

Think of it like Google Maps choosing the best route for your trip — a payment platform does the same, but for money.

Here’s how the routing actually works:

Step 1: Collecting Payment Details

The process starts when the customer enters their:

- Card information

- UPI ID

- Net banking credentials

The payment platform keeps the data encrypted and secure

Step 2: Platform Chooses the Right Payment Rail

Different transactions use different rails (paths).

For example:

- Cards: Visa, Mastercard, RuPay

- UPI: NPCI rails

- Wallets: Paytm, PhonePe, Amazon Pay

- Bank Transfers: IMPS, NEFT, RTGS

The platform decides which rail to use based on the method selected.

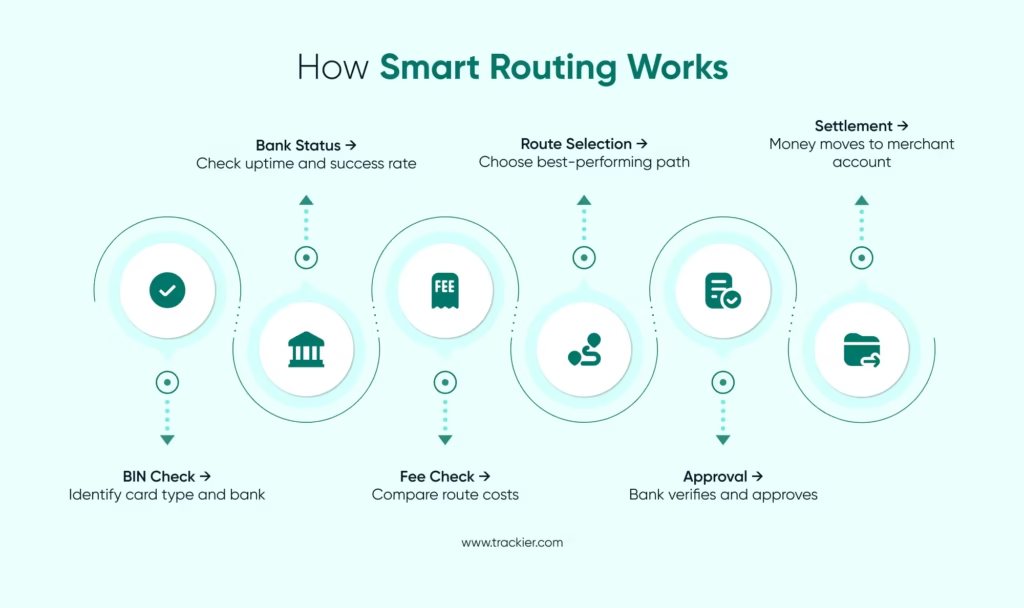

Step 3: Smart Routing

Once the method is selected, the payment platform finds the best route for a smooth transaction.

This is called smart routing

It looks at factors like:

- Bank success rate

- Real-time server load

- Network speed

- Downtime alerts

- Payment type

- Customer location

Just like how a delivery app chooses the fastest driver, the platform chooses the fastest and most stable payment route.

Step 4: Sending Data to the Issuing Bank

Now the platform sends the payment request to the customer’s bank (issuer).

The bank checks:

- Is the card or account active?

- Is there enough balance?

- Is this activity suspicious?

- Is the OTP or PIN correct?

If everything checks out, the bank approves the transaction.

Step 5: Approval or Decline

The issuing bank sends a response back:

- Approved → Payment successful

- Declined → Insufficient balance, wrong OTP, downtime, etc.

The platform shows this result instantly to the customer.

Step 6: Settlement Routing

If the transaction is successful, the platform starts settlement routing.

This means it ensures the money:

- Moves through the appropriate banking channel

- Reaches the merchant’s bank account

- Matches the right order ID

- Reflects in the merchant dashboard for accounting

Depending on the payment platform, this can be:

- Instant settlement

- T+1 / T+2 settlement

- Batch settlement

Why Smart Routing Matters?

Smarter routing = higher success rates.

Platforms use advanced algorithms to:

- Switch between banks in milliseconds

- Avoid high-failure routes

- Retry payments automatically

- Reduce drop-offs

- Improve customer experience

Many modern payment platforms use AI-powered routing that continuously learns which banks or networks work best at different times of the day.

Why Payment Platforms Matter for Businesses?

They play an important role in how businesses grow, earn, and operate. They do much more than just help companies accept money — they directly impact customer experience, revenue, and trust.

Here is why they matter more:

1. Higher Conversion Rates:

A strong payment platform increases the number of successful payments. When fewer transactions fail due to bank errors, routing issues, or slow processing, more customers complete their purchases — directly boosting revenue.

2. Better Customer Experience

Customers want payments that feel quick and effortless.

A good platform supports multiple methods (cards, UPI, wallets) and processes payments within seconds, creating a smooth checkout experience that encourages repeat purchases.

3. Reduced Fraud and Chargebacks

Modern payment platforms use AI, risk rules, and authentication tools to stop fraud before it happens.

This protects both the business and the customer.

4. Faster Settlements and Cash Flow

Timely settlements help businesses manage operations, pay vendors, and maintain healthy cash flow.

Instant or T+1 settlements allow companies to access money quickly instead of waiting for days.

5. Compliance and Security Made Easy

A payment platform handles complex security requirements like PCI-DSS, tokenization, and encryption.

This means businesses don’t need to invest in heavy compliance systems — everything stays secure by default.

6. Support for Global Expansion

Payment platforms enable international transactions with multi-currency support and local payment methods.

A business can instantly sell to customers in different countries without building its own global payment system.

7. Lower Operational Work

Payment platforms automate manual tasks like reconciliation, refund processing, and reporting.

This reduces workload for finance and support teams and helps businesses run more efficiently with fewer errors.

Modern Features That Make Payment Platforms Smarter

Today’s payment platforms are built to do much more than process money. They use automation, AI, real-time decision-making, and seamless integrations to improve success rates, protect users, and reduce operational headaches.

These smarter features help businesses accept payments smoothly and grow faster without worrying about technical complexity.

Below are the modern features explained with more clarity and depth:

1. Real-Time Payments

Real-time payments allow money to move instantly between customers and businesses. This matters because today’s users expect fast transactions — one delay and they abandon the payment.

Why it’s important:

- Customers don’t wait for bank approvals

- Businesses get money immediately (great for cash flow)

- Better experience for mobile-first users

Real-time processing is the backbone of UPI, instant wallets, and modern card approvals.

2. Tokenization for Safe Payments

Tokenization replaces sensitive card details with unique digital tokens.

The actual card number is never shared during the payment.

Why this is smart:

- Even if someone steals the token, it’s useless

- Supports one-click checkout

- Reduces PCI-DSS compliance work for businesses

- Makes subscription and saved-card payments more secure

This is why platforms like Stripe, Apple Pay, and Google Pay use tokens by default.

3. AI-Based Fraud Detection

Fraud is getting smarter — so payment platforms are too.

AI reviews each transaction in real time and detects unusual patterns.

AI checks signals like:

- User’s device type

- IP address and location

- Previous behavior

- Transaction speed (bots vs humans)

- Velocity (too many attempts)

- Known fraud patterns

Benefits:

- Stops fraudulent payments automatically

- Reduces chargebacks

- Let’s have genuine users pay without friction

AI makes security stronger without making the checkout slower.

4. Smart Routing for Higher Success Rates

Not all banks and processors perform the same every minute.

Smart routing finds the best-performing route at that moment.

How it works:

- Checks the bank’s uptime

- Reviews previous success rates

- Evaluates network loads

- Compares fees

Then it picks the fastest and most reliable path.

Why businesses love this:

- Fewer payment failures

- More successful orders

- Better user experience

- Higher revenue without marketing spend

This is one of the most valuable modern features.

5. Payment Orchestration (Manage Multiple Gateways)

Big businesses don’t rely on one payment gateway anymore.

Payment orchestration connects multiple gateways, banks, and processors into one unified system.

What it allows businesses to do:

- Failover routing (if one gateway is down, payment moves to another)

- Reduce costs by comparing fees

- Accept more international methods

- Apply custom rules for different countries

- Track all payments in one place

This makes the payment system stronger, flexible, and prepared for any downtime.

6. Developer-Friendly APIs

APIs are like building blocks that allow businesses to create their own payment experience.

What APIs allow:

- Custom payment pages

- In-app payments

- Automated refunds

- Automated payouts

- Custom UI/UX

- Integration with CRM or ERP systems

Developer-first platforms grow faster because they fit into any business model.

7. Multi-Currency & Cross-Border Support

Businesses today sell worldwide — and payment platforms support that.

What this includes:

- Accepting 50+ currencies

- Showing localized prices

- Handling FX conversion

- Connecting with international banks

- Compliance with global regulations

This helps even small businesses look and operate like global brands

Final Thoughts

Every online payment you make — whether buying groceries, watching a movie, or depositing on a gaming app — passes through a payment platform.

They silently power the world’s digital economy, ensuring payments are:

- Fast

- Safe

- Secure

- Reliable

And as technology grows, payment platforms will become even more intelligent, faster, and deeply integrated into our daily lives.

Choosing the right payment platform helps businesses grow faster, reduce failures, improve user experience, and build trust with customers.

Online payments may look simple on the front end, but behind the scenes, payment platforms are working tirelessly every second to keep everything running smoothly.

Help Centre

A payment platform is a system that helps businesses accept, process, secure, and settle digital payments. It collects payment details from the customer, routes the transaction through banks or payment networks for approval, applies fraud and security checks, and finally settles the money to the business’s account within a defined time.

No, a payment gateway is only one part of a payment platform. A gateway securely captures payment information, while a full payment platform also handles processing, routing, fraud prevention, compliance, settlements, reporting, and analytics. Platforms offer an end-to-end payment solution.

Payment platforms use multiple security layers such as encryption, tokenization, PCI-DSS compliance, and AI-based fraud detection. Sensitive data is never stored in raw form, and every transaction is monitored in real time to prevent fraud and unauthorized access.

Businesses use multiple platforms to reduce downtime, increase payment success rates, and optimize transaction costs. If one bank or gateway is down, smart routing allows payments to shift automatically, ensuring smooth transactions and a better customer experience.